Download Full Report as a PDF>>

Health Metrics

The 2020 Recession has been the result of a health crisis and the health metrics will continue to determine the speed at which the Washington region’s economy recovers. Specifically, changes in consumer behavior in reaction to the abating health crisis will lead to increased economic activity. These changes are likely to be driven by vaccination rates in the upcoming months, in contrast to the recent trends that were in reaction to COVID-19 case rates.

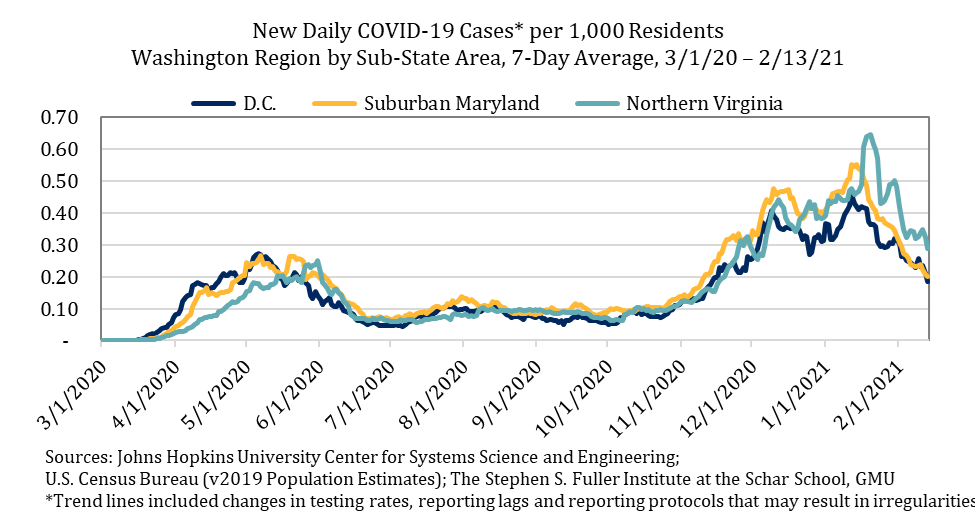

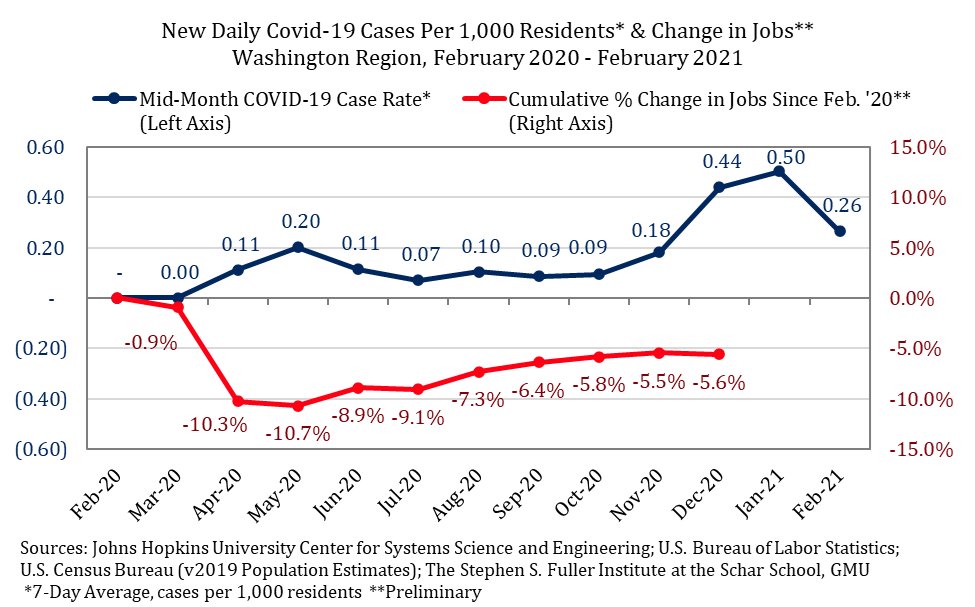

In March 2020, consumers drastically reduced their daily activities and discretionary purchases in anticipation of the pandemic. In the Washington region, this shift began prior to the first wave, as it did in many places in the U.S., and consumer spending decreased sharply by the end of March. As it became clearer that COVID-19 trends varied in different parts of the U.S., consumers appeared to shift their focus towards their local COVID-19 rates and the consumer patterns that emerged in May reflected these local conditions. In the Washington region, the first wave of the pandemic occurred from late March through the end of May. Job losses peaked in May 2020 and, as the first wave subsided, the economy improved modestly. The second wave of COVID-19 began in the Washington region in early November 2020. The economic recovery stalled in October, likely in anticipation of this second wave and due to the onset of colder weather. The economic recovery continued to lag in November before pulling back in December 2020 as case rates neared their peak; the Washington region lost 3,800 jobs (-0.1%) between November and December. The case rates in the Washington region peaked in mid-January and initial data suggest that the economy did not register significant gains in January.

As of mid-February, COVID-19 case rates in the Washington region have decreased by more than one-half (-56.3%) compared to their mid-January peak and the downwards trend has been sustained. While this improvement will help spur the economic recovery, vaccination rates will likely play a larger role in the economic recovery going forward. In the Washington region, the economic recovery in the summer was relatively modest compared to that in other areas with comparable COVID-19 trends, suggesting that consumers in the region were somewhat less likely to change their behavior in reaction to this improvement. While this also led to a relatively smaller economic contraction in December, it suggests that a large share of local consumers will wait to resume prior behaviors until their households have been vaccinated.

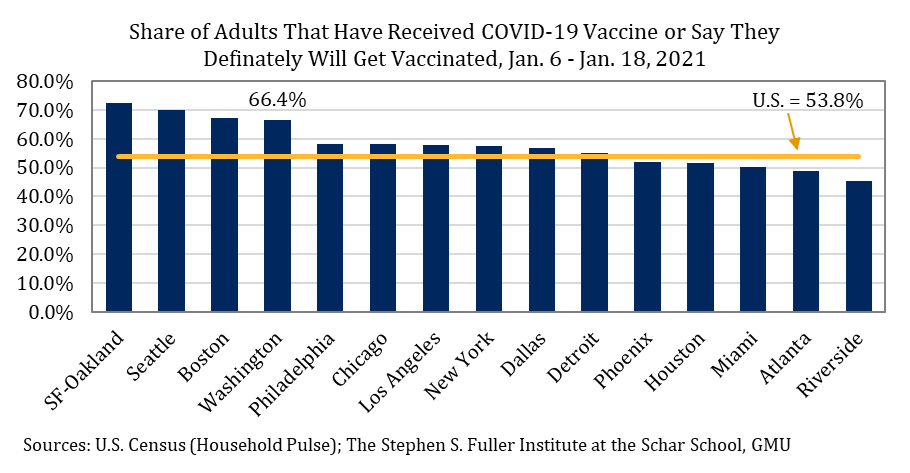

Additionally, adults in the Washington region are more likely to say that they definitely will get vaccinated or are already in the process of doing so compared to the U.S. average. As of early January 2021, 66.4 percent of all adults in the Washington region responded that they were certain that they would get vaccinated; nationally, just 53.8 percent were certain that they would or were doing so. Of the 15 most populous metropolitan areas, the Washington region had the fourth largest share of adults that were certain about their desire to be vaccinated. An additional 20.1 percent of adults in the Washington region responded that they would probably be vaccinate and just 13.5 percent of adults in the Washington region responded that they probably or definitely not be vaccinated or not respond to the question; nationally, this share was 23.0 percent.

Altogether, the improvement in COVID-19 case rates in February is likely to result in a modest increase in economic activity, similar to what occurred in the Washington region during the summer of 2020. As vaccination rates increase, the economic recovery will accelerate, but the full recovery will not occur until the Washington region’s population is vaccinated at rates that are at, or near, herd immunity levels, as determined by the health experts.

Economic Activity

The Washington region’s economy reached its trough in May 2020, during the peak of the first wave of COVID-19. Compared to its pre-pandemic peak in February 2020, the region lost 362,900 jobs for a decline of 10.7 percent. Between May and September 2020, the region recovered 146,500 jobs, or about two-fifths of all the jobs that had been lost. The jobs recovery slowed during the fall and the region recovered 31,300 jobs between September and November 2020, before losing 3,800 jobs in December. This reversal occurred as the second wave of COVID-19 surpassed the case rates that occurred during the peak of the first wave in the Washington region and the colder winter weather made outdoor activities less viable. As of December 2020, the region had recovered 174,00 (48%) of the jobs that were lost in the April and May 2020, on net.[1]

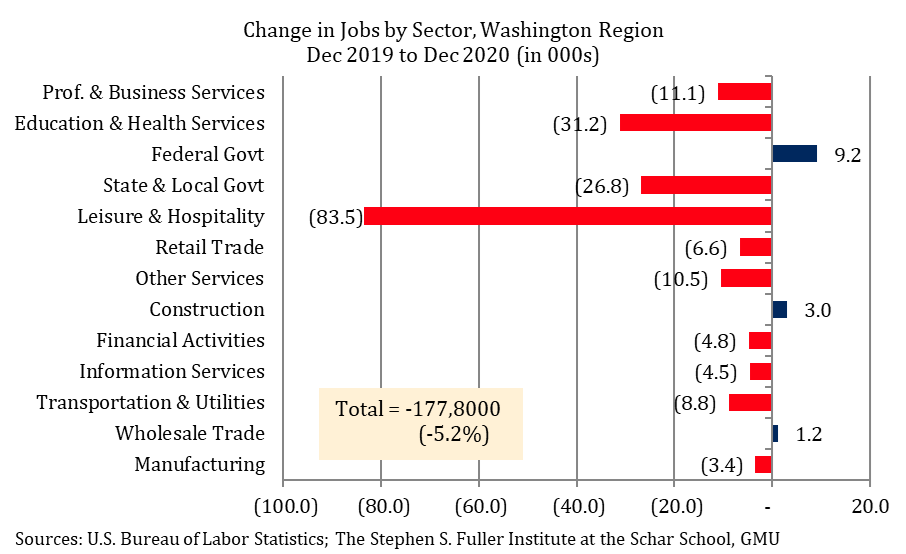

Compared to December 2019, the Washington region had 177,800 fewer jobs for a decrease of 5.2 percent. The losses continued to be largest for the Leisure & Hospitality sector, which had 83,500 fewer jobs and one-quarter (25.0%) of the jobs in this sector were lost at the end of the year compared to 2019. This sector also had the largest reversal in gains in December; in November, the monthly over-the-year decline was 22.4 percent. Within this sector, the Accommodations sub-sector had the largest losses in December 2020, decreasing by 39.4 percent compared to last December. The Arts, Entertainment & Recreation sub-sector had 28.2 percent fewer jobs, while the Food Services & Drinking Places sub-sector had 21.7 percent fewer jobs.

The sector with the second largest absolute jobs losses as of December 2020 was Education & Health Services, which had 31,200 fewer jobs (-6.9%). The losses in this sector were largest for non-hospital health care services (-8.2%). Private sector Education Services decreased by 7.0 percent between December 2019 and December 2020, while the number of jobs in hospitals decreased by 2.3 percent. On a percentage point basis, the second largest loss was in the Transportation & Utilities sector, which decreased by 11.1 percent (-8,800 jobs) between December 2019 and December 2020. These losses were likely concentrated in the transportation sub-sector, although the data on this sub-sector have not yet been released.

As of December, three sectors and one key sub-sector had job growth compared to last December. The Federal Government did not have job losses during the pandemic. During the summer months, the gains were bolstered by temporary Decennial Census workers. By December, these workers were off payrolls and the monthly over-the-year gain of 9,200 jobs (+2.5%) reflects more sustained gains. The Construction sector recovered from the pandemic in October 2020 and had 3,000 (+1.8%) more jobs in December 2020 compared to the prior year. This sector has yet to fully recover from the 2008 Recession, however, and this sector had 25,700 fewer jobs compared to its December-peak in 2005. The third major sector with gains was Wholesale Trade, which also recovered from the pandemic in October. As of December 2020, this sector had 1,200 more jobs (+1.9%) compared to last December. Lastly, the major sub-sector that had gains was the Professional, Scientific, & Technical Services & Management sub-sector, which is in the Professional & Business Services sector. This sub-sector accounted for 17.1 percent of the region’s jobs in 2019 and is a key driver of the region’s economic activity. During the pandemic, this sub-sector continued to add jobs and increased by 5,600 jobs (+1.0%) between December 2019 and December 2020.

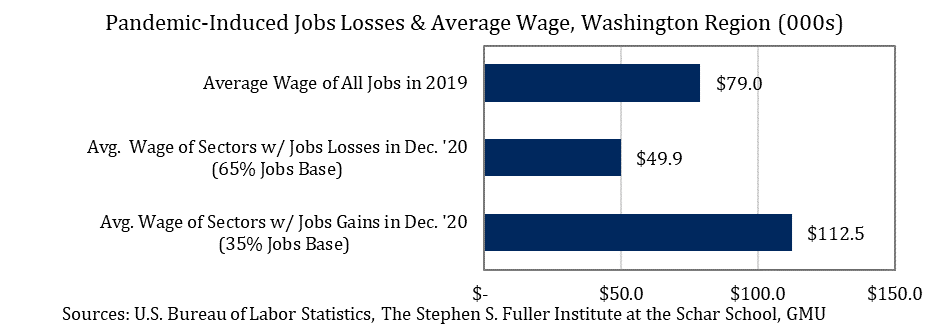

The sectors and key sub-sector that had monthly over-the-year gains as of December 2020 accounted for 34.8 percent of the Washington region’s jobs base in 2019. The average wage of these jobs was $112,540 and was 42.4 percent larger than the average wage of all jobs in the Washington region in 2019. By contrast, the sectors with the largest losses had relatively low average wages. Overall, the average wage of a job that was lost during the pandemic as of December 2020 was $49,900, which is 36.8 percent smaller than the average wage of all jobs. This uneven pattern of losses and recovery will continue in the upcoming months and many low wage sectors will not fully recover until 2022.

Near-Term Outlook

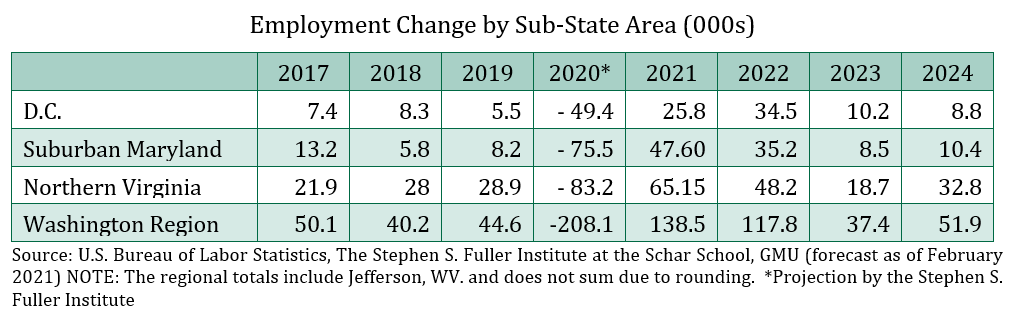

The Washington region’s economic recovery has lagged since the fall of 2020 and is likely to continue to do so until March 2021, when the rate of recovery is projected to increase. The improvement this spring will be the result of three key factors: the end of the second local wave of the pandemic, the improvement in weather that will allow for more outdoor activities, and the continued increase in vaccination rates. The increase in vaccination rates will further accelerate the economic recovery later in 2021, resulting in the recovery of a projected 138,500 jobs, or about two-thirds (66.5%) of all the jobs that were lost in 2020. None of the sub-state areas are projected to fully recover their jobs in 2021. Instead, the full recovery in jobs is projected to occur in 2022 for the region and each of the sub-state areas. In 2022, the region is projected to add 117,800 jobs, or an increase of 48,300 jobs compared to 2019. In 2023, the majority of the sectors in the Washington region are projected to have recovered from the pandemic and will need to generate new business plans separate from those of the 2020-2022 period, which were affected by the pandemic. As a result, the region is projected to add 37,400 jobs in 2023, an increase that is in line with the long-term annual average change prior to the pandemic of 38,840 but smaller than the gains during a typical business expansion. Growth in 2024 is projected to strengthen and the region is forecasted to add 51,900 jobs, an increase that is similar to the post-Sequestration business expansion pattern in 2015-2017.

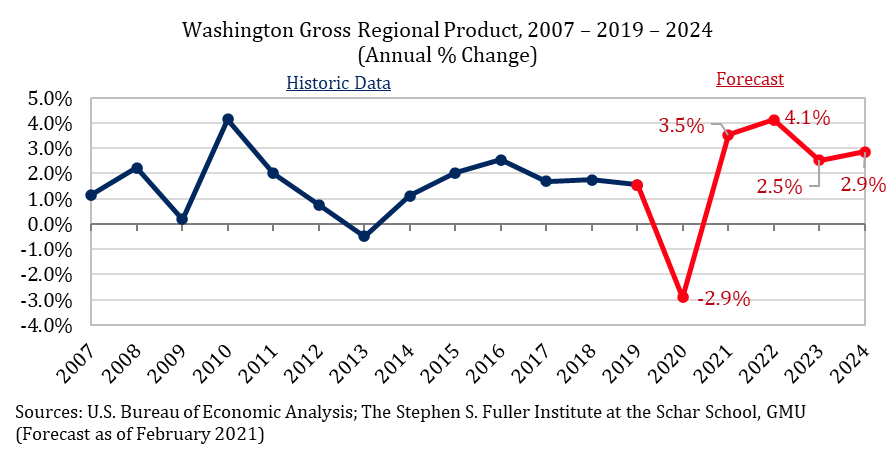

Total economic activity in the Washington region, as measured by its Gross Regional Product (GRP), is projected to have decreased by 2.9 percent in 2020. This decline is larger than any on record, with data beginning in 1990.[1] Total economic activity is projected to recover in 2021, with a GRP increase of 3.5 percent. In part, the GRP recovery in 2021 is the result of activities that are less tied to job growth, including business investment and increased inventories. Still, the GRP gain in 2022 is projected to be larger than the improvement in 2021 and GRP is forecasted to increase 4.1 percent. The increase in economic activity in 2023 is projected to moderate and GRP is forecasted to increase 2.5 percent, reflecting the repositioning to a post-pandemic economy. In 2024, GRP is forecasted to accelerate, increasing 2.9 percent.

These forecasts continue to be subject to more uncertainty than in past years. Consumer sentiment, in particular, will play an outsized role in how the Washington region recovers. Consumer confidence in present conditions has yet to have sustained improvement as of January 2021 and consumer expectations in future economic conditions continued to worsen, suggesting that residents are increasingly affected pandemic fatigue. If consumer sentiment does not improve in the spring, as the weather improves and the second wave of COVID-19 subsides, then the economic recovery in the Washington region will be slower than what is currently forecasted. Another factor that may slow the recovery includes a slower return to the labor force by the region’s residents. During the pandemic, a large number of residents in the Washington region left the labor force after losing their jobs. Most of these potential workers will return to the labor force when jobs become more readily available, but the timing and the potential for a permanent loss of labor may further subdue the recovery in 2021.

About These Data

Data on confirmed COVID-19 cases are from the Johns Hopkins University Center for Systems Science and Engineering and aggregated by county to the 2013 Metropolitan Statistical Area definitions. Payroll jobs data and employed residents data are from U.S. Bureau of Labor Statistics. Data on intent to be vaccinated are from the U.S. Census’s Household Pulse Survey, microdata file. Consumer confidence and expectations are from the Conference Board for the South Atlantic region. The Washington region’s forecast is based on estimates by the Stephen S. Fuller Institute. All data are as of 2/14/2021.

[1] These month-to-month changes are seasonally adjusted.

[2] Historic GRP data are from IHS Markit.