Download Full Report as a PDF>>

The 2020 economic recession is the result of the COVID-19 pandemic; activities that were previously safe became higher risk, or had higher uncertainty about their safety, and consumers and businesses changed their behavior in response. This health crisis is not yet resolved and its trajectory will continue to be the main factor in the economic recovery. Similarly, the improving understanding about which activities pose the highest risk and actions that can be taken to mitigate risk will continue to alter consumer and business preferences.

Consumer spending decreased as a result of the health crisis and these losses rippled through the economy, decreasing economic activity. The decrease in local consumer spending was largest for discretionary items that had a higher degree of person-to-person interaction, like travel and restaurants. Large losses also occurred in transportation spending as the result of teleworking and overall declines in mobility.

Because of the decline in consumer spending and the overall uncertainty that resulted from the pandemic, the Washington region lost 10.7 percent of its jobs between February 2020 and May 2020, after adjusting for seasonal patterns. The total decrease in jobs during the pandemic was more than three times as large and occurred 6-8 times more quickly than during the 1990 and 2008 recessions. Between May and August 2020, the region recovered about 35 percent of the jobs lost, led by the Retail Trade and Leisure & Hospitality sectors. Even with this improvement, the job losses as of mid-August remained more than twice as large as those during the 1990 and 2008 recessions. Additionally, these jobs losses do not capture the three major shifts in the economy that are unique to this pandemic:

- A significant number of workers in the Washington region are now working from home. More than one-half (54.4%) of all households in the Washington region have at least one worker teleworking because of the pandemic, a rate that is larger than any other large metro. While this has likely helped preserve jobs and economic activity, teleworking will likely slow the recovery in some consumer services and the transportation industry.

- The economic productivity per job decreased in the second quarter of 2020 for most major sectors of the national economy. This decrease indicates that the underlying economic situation was worse than the jobs data reflect.

- About 20-30% of workers that lost a job in the Washington region during the pandemic left the labor force. Some of these workers left because the pandemic affected their jobs directly and they are likely to return when the job market improves. However, a large number of former or potential workers are not interested or unable to work because of concerns about getting or spreading the virus or because they are the taking care of children that are not in school or daycare. These workers will not return to the labor force until the health crisis has abated and the systems, like childcare and transportation, are fully operational.

For the remainder of 2020, the economic recovery will continue to moderate. Concerns about a second wave of the pandemic will slow consumer spending. These concerns will be compounded by the upcoming election and the uncertainty about both the results and the potential for a prolonged ballot count. Regional businesses and households will likely postpone major decisions until after the results are known. In January, assuming that the election results are known and that the pandemic trends relating to colder weather are established, the economic recovery will accelerate modestly. This acceleration will primarily consist of economic activities that were postponed during the fall and not constitute a fundamental shift in the recovery path. Instead, the overall rate of recovery will not permanently accelerate until there is a vaccine that is widely distributed. In this forecast, a vaccine is assumed to be available in the middle of 2021 and assumed to be commonly available. As a result of these assumptions, the full economic recovery occurs in 2022.

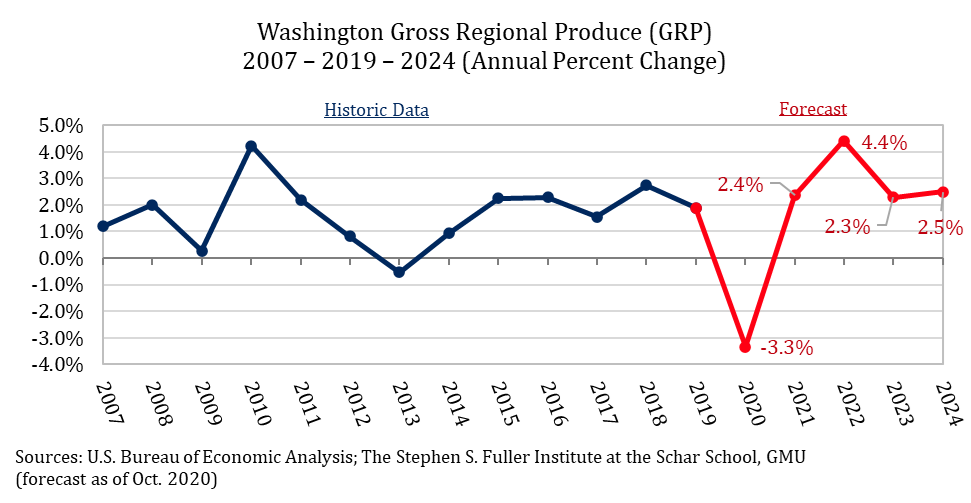

The Washington region’s economy, as measured by its Gross Regional Product (GRP), is projected to decrease by 3.3 percent in 2020. This is the largest decrease on record, with data going back to 1990. Economic growth in 2021 is projected to be 2.4 percent, with the strongest gains in the second half of the year. The largest economic rebound will occur in 2022, after the vaccine is presumed to be available and in use. During 2022, businesses and households are forecasted to fully catch-up on the forgone economic activities of the prior two years. In 2023, economic growth will slow to 2.3 percent because the majority of the catch-up activity will have occurred. By 2024, the Professional & Business Service sector is projected to have large gains as this sector pivots away from the pandemic-economy and returns to its pre-pandemic trend of diversifying away from the Federal Government.

These economic projections are subject to more uncertainty than in past years and a change in the trajectory of the pandemic or the timing and distribution of the vaccine will significantly alter these forecasts. In this scenario that assumes no local second wave of the pandemic and a vaccine by mid-2021, the economy will return to its 2019 level in 2022, a loss of economic growth for two full years. If there is a second wave locally or if the vaccine is not widely available by the middle of 2021, this recovery will be delayed further.