Download “The Effect of the Coronavirus Pandemic on the Washington Region’s Economy” as a PDF

The coronavirus pandemic has ended the longest business expansion on record, although the information that confirm this will not be available for several months.[1] Unlike prior business cycles, the Washington region’s economy is not disproportionately insulated from its effects and will mirror the trajectory of the U.S. Based on a scenario in which the coronavirus affects normal operations through May 2020, the national economy is projected to contract 0.2 percent in 2020 and the Washington region’s economy will stall, increasing by 0.1 percent for the year. The effects will be most pronounced for service industries that rely on discretionary spending and those that have strong international ties, especially business that rely on international manufacturing.

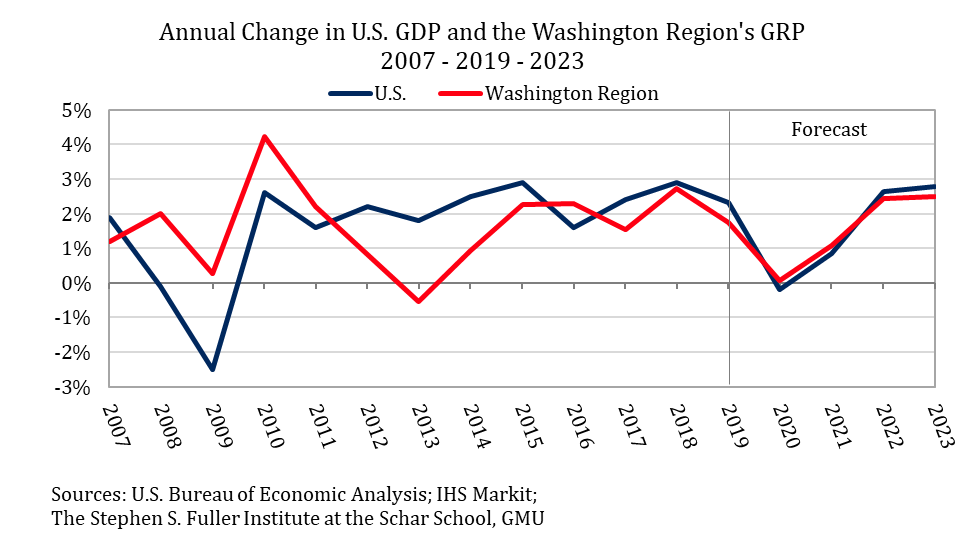

I. Gross Domestic Product & the Washington Region’s Gross Regional Product

As a result of decreased demand from both domestic and international consumers and declines in productivity, IHS Markit projects that the national economy will contract by 0.2 percent in 2020. The sharpest decline will be in the second quarter of 2020, when the seasonally adjusted gross domestic product (GDP) will decrease 5.4 percent.[2] The economic decline moderates for the remainder of the year, decreasing 2.4 percent in the third quarter and 1.5 percent in the fourth quarter. Economic activity is projected to rebound in the first quarter of 2021, rising 3.3 percent, when households and businesses resume normal spending patterns and partially compensate for the lost expenditures in the past year.

The Washington region’s economy will also contract in the last three quarters of 2020, primarily because of decreased consumer spending and lost productivity. The Washington region’s businesses are modestly less dependent on international manufacturing and are better positioned for their workers to work remotely, so the pattern of economic decline differs slightly. The Washington region’s performance will be similar to most of its peer metros, which are typically knowledge-based economies, and its role as the national capital will not insulate it from the majority of coronavirus’s economic effects. In a typical recession, the federal government is a stabilizer for the region by being a consistent, or growing, source of income for a significant share of local business and households. In turn, these federally dependent businesses and households spend money at other local businesses, supporting secondary activities even during a business cycle downturn. In this downturn, households and business will reduce expenditures at local businesses even if their incomes are unchanged as households, business, and governments implement strategies to flatten the curve of the pandemic. Similarly, the loss of productivity in the region will be because of workers that stay home, including losses from those that have shifted to working remotely. Federal workers and contractors will have the same difficulties working remotely as other office workers, in aggregate, especially because security requirements will preclude many from performing their normal tasks.

The sharpest decline in the Washington region’s economy, as measured by gross regional product (GRP), will occur in the second quarter of 2020 (-3.8%). GRP in the third quarter will decrease 1.2 percent at a seasonally adjusted annual rate and the losses in both the second and third quarters will be modestly smaller than those for the nation overall. GRP in the fourth quarter will decrease 0.9 percent and the regional economy will outperform the U.S. by a smaller margin because of the historic pattern of deferred activity prior to a national election. However, the Washington region’s recovery from the pandemic will be somewhat stronger compared to the U.S. as a result of the outsized role of the federal government in the region. The source of funding and the workforce of the federal government and federal contractors will be less affected by the disruption, making it easier for both the businesses and the associated households to resume normal operations.

Altogether, the Washington region’s GRP will increase 0.1 percent in 2020 and 1.1 percent in 2021, outperforming the U.S.’s GDP by 0.3 percentage points in each year. In 2022, the Washington region will revert to its recent trend of underperforming the national economy. Economic growth in the region is projected to be 2.4 percent in 2022 and 2.5 percent in 2023, 0.2 to 0.3 percentage points less than the nation’s growth. This underperformance is driven by the region’s economic dependence on the federal government and the private sector’s slow repositioning towards non-federal activities.

II. Tourism & Discretionary Spending

The decrease in discretionary consumer spending will be the main contributor to the economic slowdown in the Washington region, accounting for 65-75 percent of the GRP lost compared to the pre-pandemic baseline growth that was forecasted for 2020 and 2021. This will affect services industries that rely on discretionary spending, including the Leisure & Hospitality sector, the Retail sector, and the Other Services sector, which includes personal care, maintenance and in-home household services. The losses will be sharpest in the second quarter, assuming that social distancing requirements and recommendations are no longer in place by the third quarter. During this time, service industries will lose revenues from both local and non-local consumers. When service businesses can resume normal operations, local consumers will return incrementally but business and leisure travel will likely stay below its pre-pandemic levels for another 1-2 quarters.

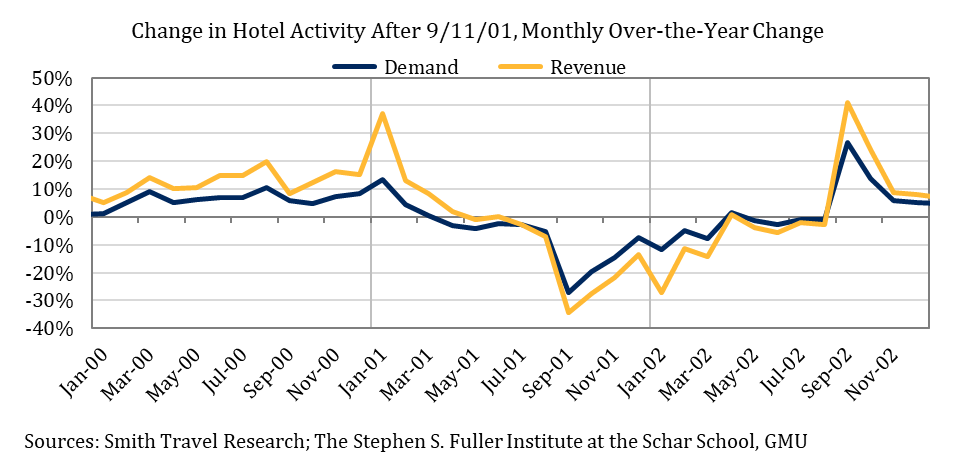

The tourism industry is typically strongest for the Washington region in the spring and would have been affected even if there were no domestic cases of the coronavirus. The domestic outbreak will reduce tourism to unprecedented levels. The most comparable recent event was the September 11, 2001 attacks, although the total magnitude of the decrease resulting from the pandemic will likely be larger. In the 12 months after the September 11, 2001 attacks, hotel revenues in the Washington region decreased 13.6 percent and the number of occupied rooms decreased 8.1 percent. If hotel performance follows this path, the total 12-month loss in revenues at regional hotels would be $630 million. The decreased spending from travelers, plus the indirect and induced effects of the lost earnings, would result in an additional $600 million of lost economic activity, for a total decrease of $1.2 billion. A decrease of this magnitude accounts for about seven percent of the GRP growth that is lost due to the pandemic in 2020 and 2021 compared to the pre-pandemic forecast and a more prolonged decrease in the early months would increase this share to about ten percent.

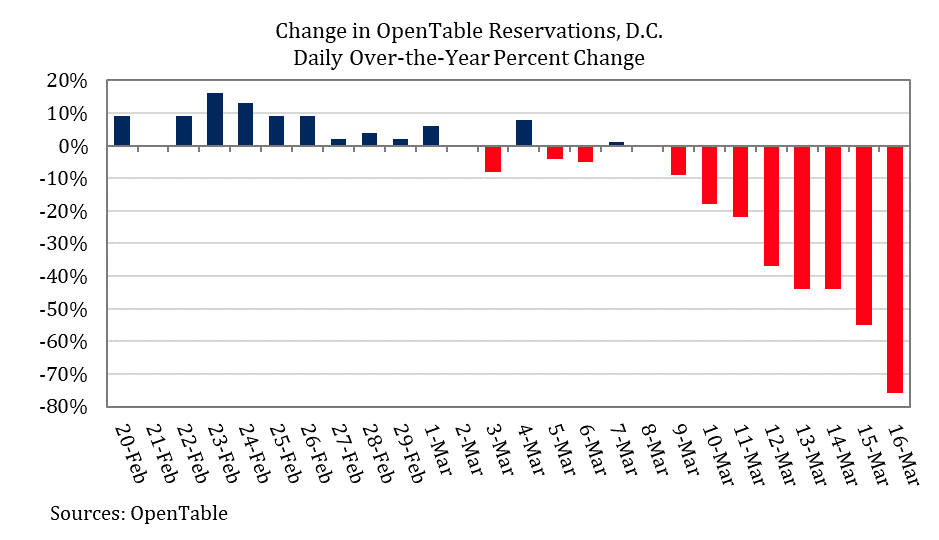

Local households will also reduce their spending on discretionary items in the next three quarters. While February and March will have stronger spending on grocery and household items, the increased spending on these non-durable goods (food, personal care items etc.) is displacing spending that would have happened later in 2020 or 2021 so the net effect over the next 12 months will be negligible. Instead, the largest difference will be the reduction in spending in restaurant, entertainment, retail and personal care services during a two- to three-month period. Unlike prior recessions, this pullback has been sharp and has occurred quickly. Data from OpenTable shows a 76 percent decrease in reservations in the District on March 15, 2020 compared to the same day in 2019, whereas the average change for the week ending on March 5 was +1.0 percent. Many service industries have likely experienced a similar decrease, although delivery services may moderate this revenue effects of this decline slightly.

Once restaurants, personal care services, and other retailers can resume normal operations, revenues from local customers will return; in this analysis normal operations resume in the third quarter. During the recovery, the pent-up demand for these services will increase local consumer spending beyond what would have occurred during a normal period, but it will not fully compensate for the lost revenue during the first and second quarters for two reasons: 1) consumers cannot double-up on some activities in a given period; residents will not get two haircuts in the fall even if they did not get their regular haircut in the spring; and 2) the net wealth of households will likely be affected because of investments and wages, particularly for service workers, which will moderate the rebound in consumption.

The workers in service industries that rely on discretionary spending will also have the largest rates of wage reductions and lay-offs and, while this will not be an outsized contributor to the region’s economic losses, it will be the largest source of unemployment and disproportionately affect lower income households. About 23 percent of residents in the Washington region work in these service industries as their main job, a total of 760,000 residents.[3] If just 15 percent of this workforce is laid-off, an additional 114,000 workers will become unemployed, increasing the region’s unemployment rate to 6.4 percent from the 2019 average of 3.1 percent.[4] If 30 percent of this workforce is laid-off, even temporarily, the additional 228,000 unemployed workers would increase the regional unemployment rate to 9.7 percent.

These service workers are also more likely to also be in low-income households and less able to compensate for the lost income through savings or wages from other household members. Of all households with any worker in a service industry, 7.5 percent had total household incomes less than $25,000 and a total of 22.5 percent had household income less than $50,000. By comparison, just 12.2 percent of households with non-service workers had total household incomes less than $50,000. As these service workers lose hours, their households will have more difficulty recovering from these lost wages.

Overall, the net decrease in consumption from the region’s residents and households will account for 55-65 percent of the overall GRP growth that is lost due to the pandemic in 2020 and 2021 compared to the pre-recession forecast and an additional ten percent will be the result of lost tourism.

III. Other Industries

Industries that do not rely on tourism or discretionary spending will be less affected by the pandemic-induced recession but there will be economic losses associated with decreased productivity. Many organizations have either mandated that their employees work from home or have encouraged them to and it is likely that more will do so in the upcoming weeks. Most workers do not have the same resources in their homes as they do at their offices so not all work will be performed as efficiently during their work-from-home periods and some work will be deferred until normal operations resume, causing economic bottlenecks.

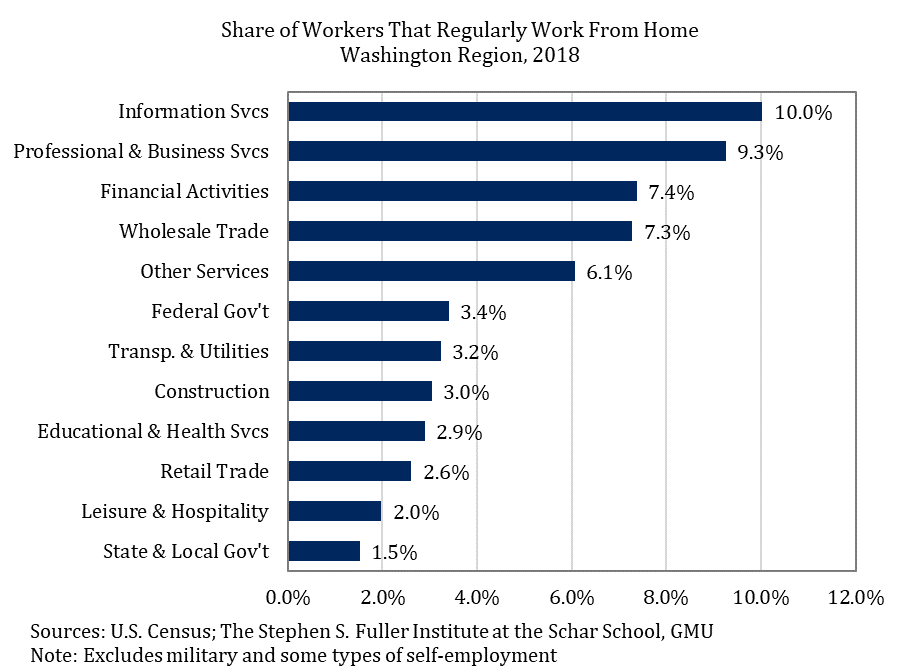

The industrial structure of the Washington region means that slightly more workers typically worked at home compared to the national average, which indicates that the regional productivity loss will be less than the nation’s. Workers that are in office-using jobs are more likely to currently work from home compared to other types of workers in the region, although the Professional & Business Services sector is less likely to typically work from home in the Washington region compared the national average, likely due to security requirements of federal contractors.

IV. Other Considerations

If social distancing measures are in place past June 2020, the economic losses will be compounded; that is, the losses will not scale proportionally with each additional month of the coronavirus pandemic. The sharp decrease in consumer spending during a one-quarter pandemic is not the result of commensurate losses in income during this period but is the result of significant decreases in consumer confidence and the inability to freely access restaurants, retailers and other service providers. The longer the pandemic continues, the more likely it is that total household income in the region will decrease significantly enough to suppress the consumer spending post-pandemic, subsequently delaying the economic recovery. Similarly, businesses will have more difficulty absorbing lost productivity over time; small business and industries that rely on discretionary spending typically operate with smaller margins and will be the first to cut costs, while larger businesses that consist of salaried workers are more able to have workers take paid leave for several weeks if work cannot be performed at home.

About These Data

The national economic forecast is from IHS Markit’s March 13, 2020 Forecast Update; IHS Markit provides national and local economic, demographic and housing forecasts. The Washington region’s forecast is based on estimates by the Stephen S. Fuller Institute. Historic hotel data are from Smith Travel Research and restaurant reservations data are from OpenTable and available here. Estimates of vulnerable services workers and their incomes are based on the U.S. Census Bureau’s 2018 American Community Survey microdata and the U.S. Bureau of Labor Statistic’s Local Area Unemployment Statistics as of March 17, 2020. Estimates for workers that regularly work from home are from the 2018 American Community Survey microdata.

[1] The leading indicators and preliminary Gross Domestic Product data should provide confirmation by the end of April. However, the organization that is most frequently used to date U.S. business cycles, the National Bureau of Economic Research, has historically taken between six and 21 months after the recession has begun to declare the end of the cycle.

[2] The quarterly seasonally adjusted annual rate (SAAR) estimates the change from the prior quarter after accounting for seasonal patterns. This is not equivalent to the quarterly over-the-year change so the average SAAR for the year does not equal the annual change.

[3] Service industries include Retail, Administrative, Support & Waste Management, Leisure & Hospitality, and Personal, Maintenance, & In-Home Services.

[4] Some of these workers would not be able to actively look for a job during their unemployment so the officially reported unemployment rate will not fully capture this change.