This is the second blog of two covering this report. In this post, we examine the potential housing impacts related to HQ2. In the first post, we look at the economic and fiscal impacts of Amazon’s HQ2 on the region.

Download the full report as a PDF>>

While HQ2 will generate additional demand for housing, its effects will be geographically dispersed and gradual. Even so, the additional demand would like increase both home sales prices and rental rates, albeit only marginally above the rise that is expected to occur without these households. The average wages of HQ2 workers indicate that many of these households would be able to afford new construction, both ownership and rental housing. Additional supply would mitigate any price increases that would occur for the existing housing stock.

The housing impacts will be geographically dispersed and gradual.

Even with all the workers concentrated in one location, the workers and their households will be dispersed throughout the region, as are those who currently have a job in Arlington County, VA. No single jurisdiction will house all of the HQ2 employees, as these workers will have differing preferences and household types.

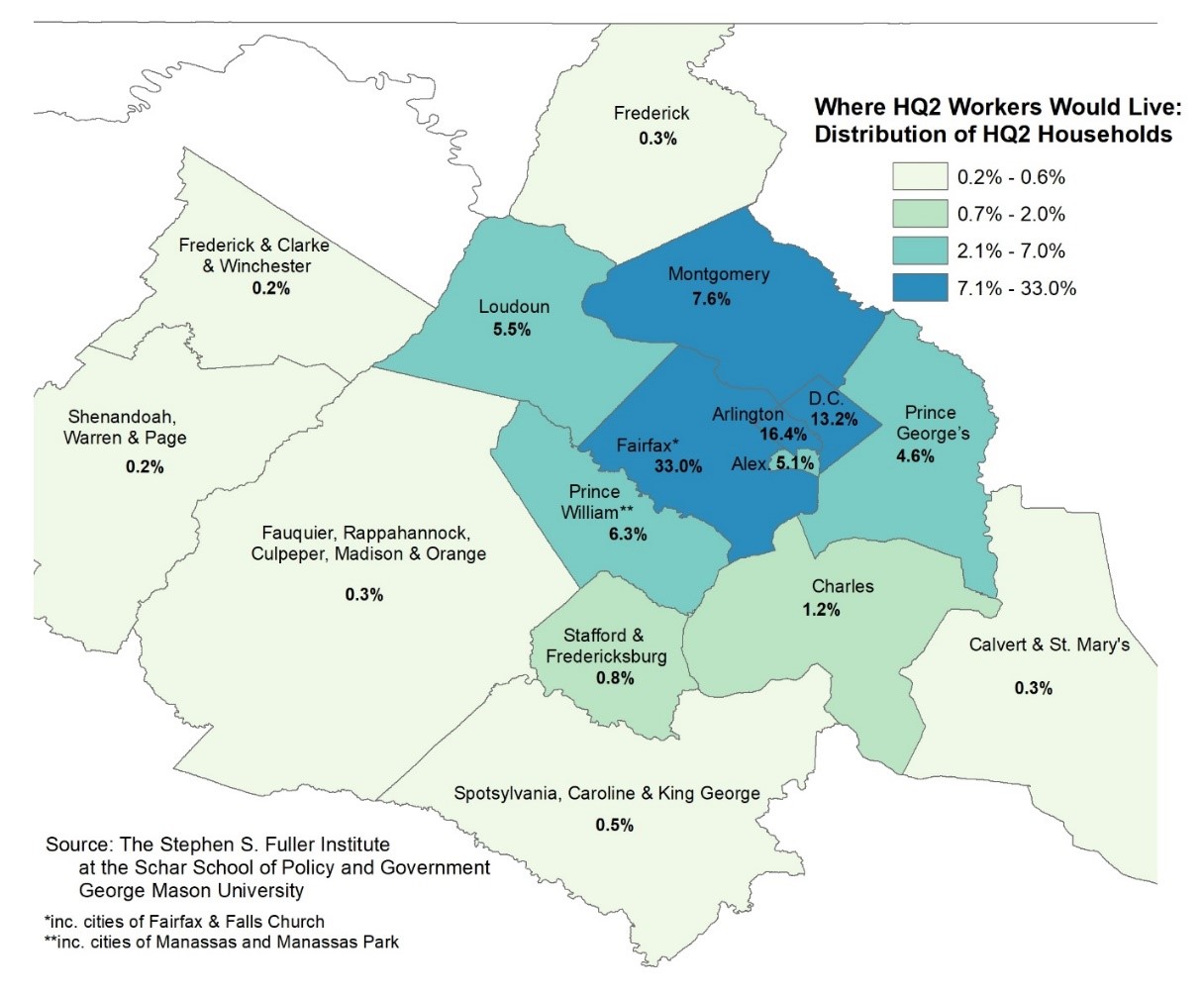

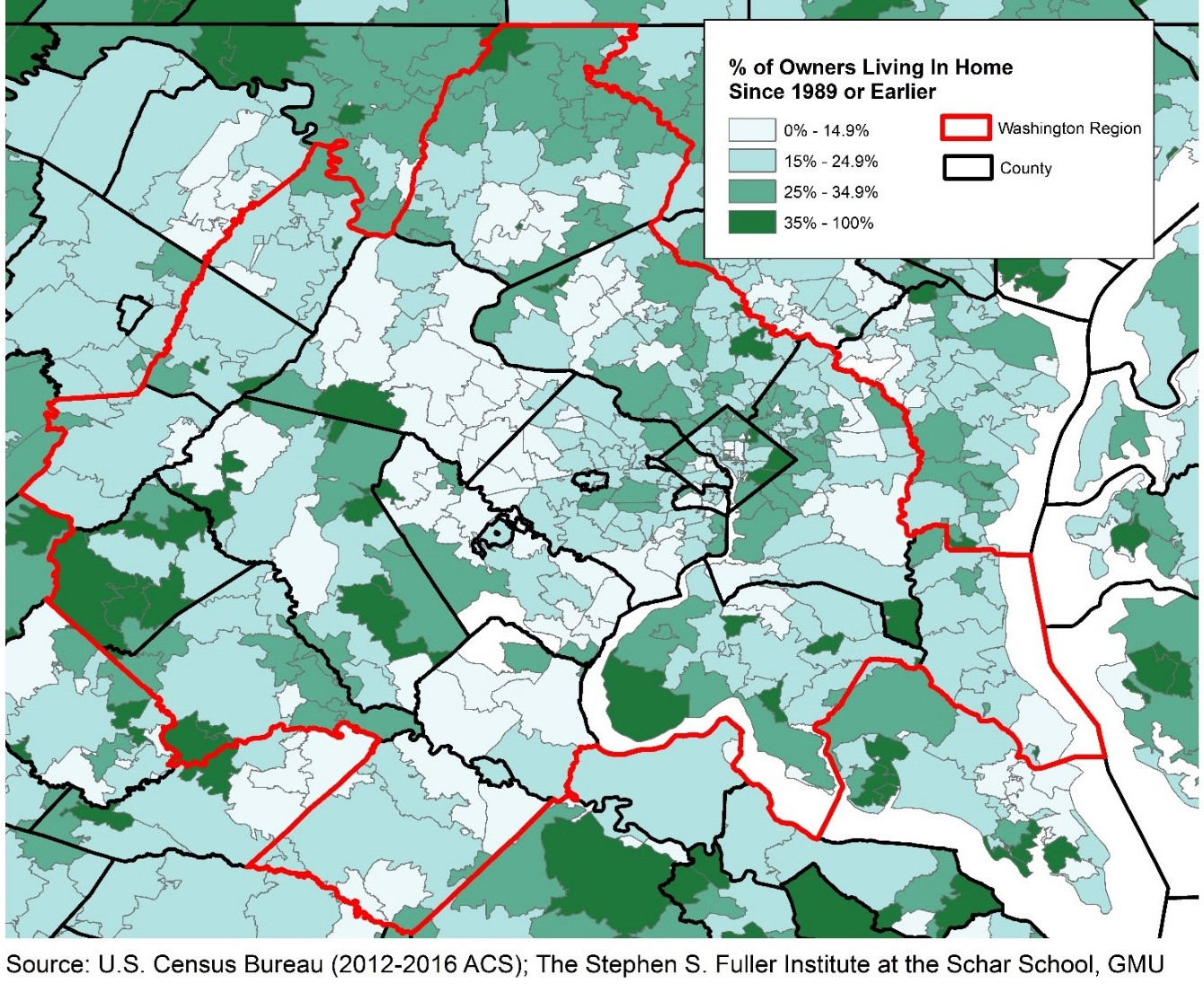

Because of the likely age and income distribution of the HQ2 workers, an estimated 14-16 percent are likely to live in the County, based on the current patterns of workers in the County. The majority (93-95%) are likely to live in the Washington region. The map below shows the distribution of households with an HQ2 worker, assuming that the HQ2 jobs have an average wage of $150,000.

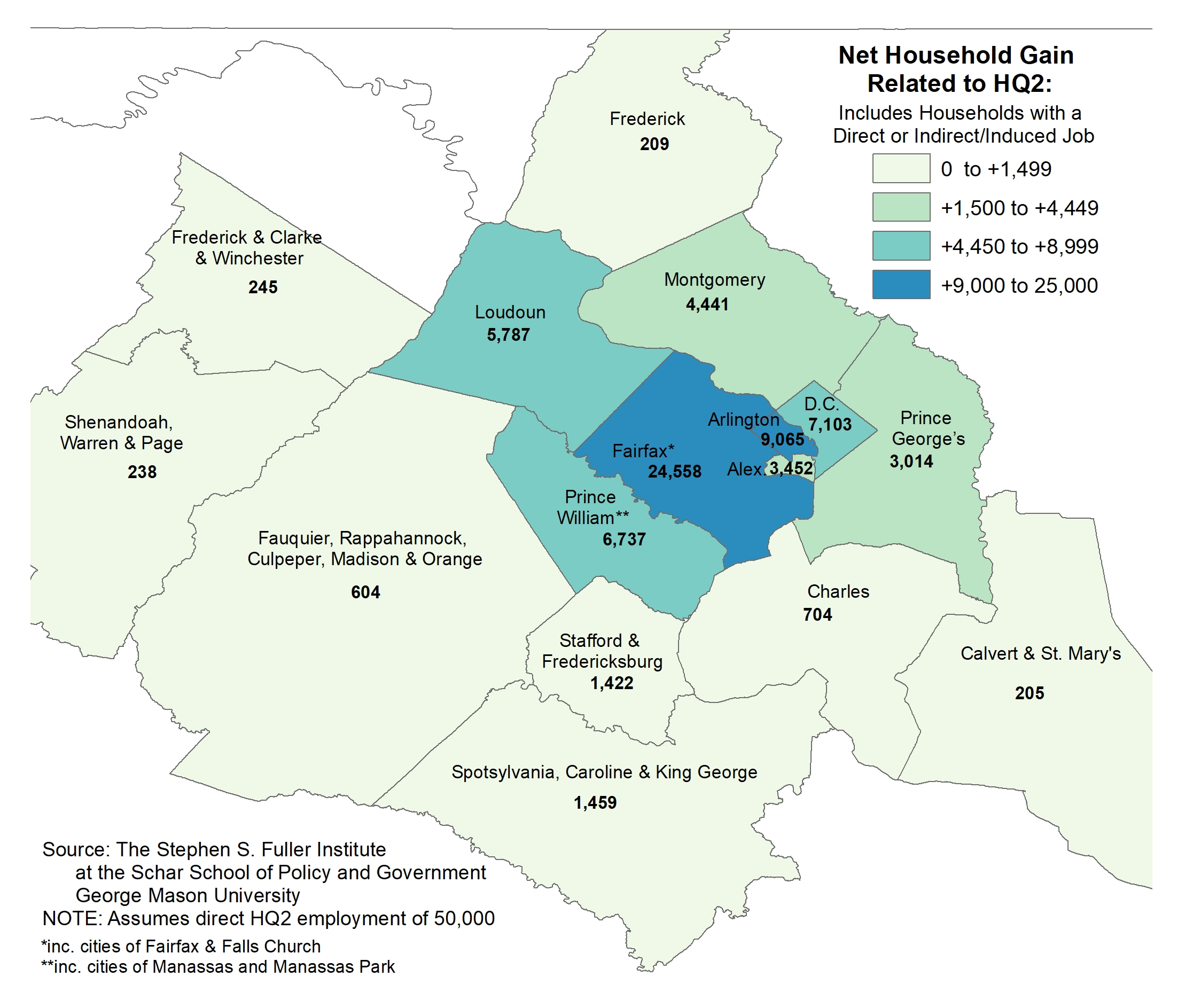

Including the household growth that results from indirect and induced jobs located in the Commonwealth, the increased demand for housing remains relatively modest. The total increase at full build-out is shown on the next page. These households will arrive or form gradually, and most increases would be well within the expected gains that these jurisdictions have been planning to accommodate, even prior to the announcement of HQ2.

Overall, HQ2 would increase the demand for housing in the Washington region. However, this demand would be relatively dispersed in the region and occur gradually, allowing jurisdictions to plan for the increase or adjust their current plans as needed.

Home prices will likely continue to rise, but the Amazon-specific increase will be difficult to isolate.

Whether or not the households shown in the maps above ultimately live in those jurisdictions will be contingent upon these jurisdiction’s abilities to create new housing at the price points that these households can afford. Given the average wages of these households and their likely household sizes, many will be able to afford new construction, potentially mitigating the effects of their increased demand on housing prices for existing residents if the jurisdictions continue to build additional housing.

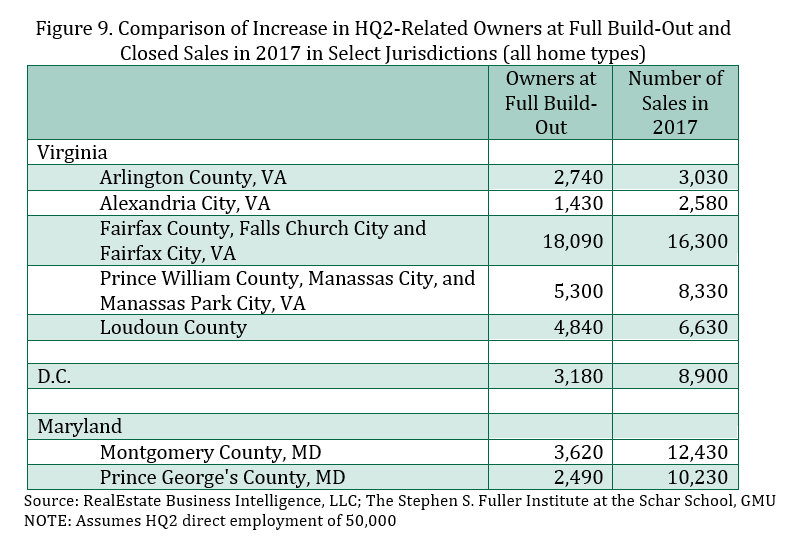

In terms of the overall change in demand in from net new owner households resulting from HQ, most jurisdictions typically have more turn-over in existing homes in a single year than HQ2 would generate during the 20-year build-out (Figure 9). While HQ2 would certainly increase the demand for ownership housing, especially in the long-term, the increase would relatively small compared to the typical demand for housing in these jurisdictions.

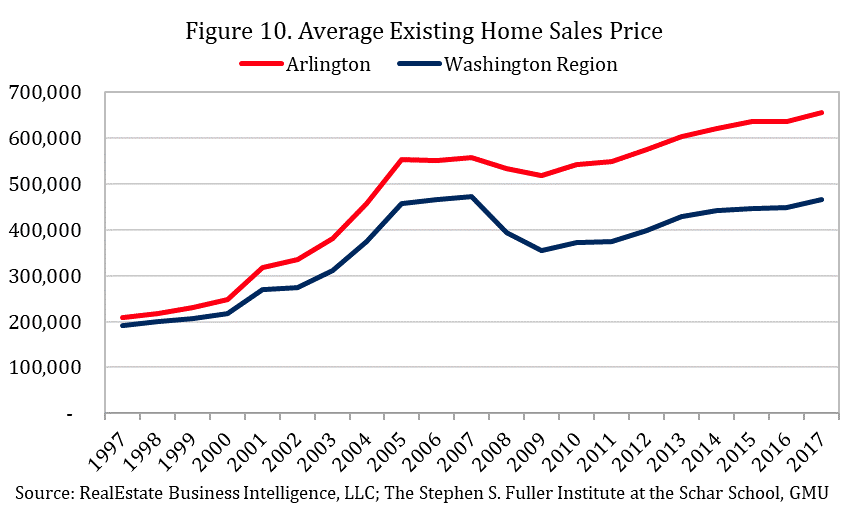

In the past 20 years, the average sales price of an existing home in the Washington region increased 143 percent and the price in Arlington County, VA increased 215 percent (Figure 10). The overall increase in the region has been driven by the net gain of 866,000 jobs (+36%), 1.6 million residents (+35%) and changing land values, more broadly. Amazon’s HQ2 is projected to add up to 50,000 jobs, directly, and up to 205,000-214,000 net new residents, including both the direct and secondary impacts. The maximum HQ2-related change, is the equivalent to 6-13 percent of the employment and population growth that occurred in the past 20 years and would likely have contributed a similar share of the home price appreciation during that time.

While the HQ2 metrics indicate the degree of demand that it could generate, the supply of homes will also play a key role in determining future pricing. New home construction in the Washington region, while improving, continues to lag historic norms. If this pattern continues, housing prices may continue rise faster than in the past relative to household growth, with or without HQ2. Builders may see HQ2 as an opportunity and increase production as a result.

Alternatively, demographic factors may play a moderating role in home price appreciation going forward. HQ2 growth is projected to occur during a period of unusually large housing market turn-over. Baby Boomers account for approximately two-fifths of all home owners in the Washington region and many of these owners have had their home for more than 20 years. As this generation retires and potentially downsizes either in the region or elsewhere, the supply of homes on the market would increase. The increase in supply and the type of supply (predominately older and potentially un-renovated) could moderate price gains, especially in some neighborhoods at some price-points.

The households related to Amazon’s HQ2 will increase the demand for ownership housing. If supply constraints continue, prices will likely rise faster than historic norms, although a relatively small share of this rise would be HQ2-specific. Demographic patterns may play a role in moderating these gains.

Similarly, rental rates will likely continue to rise, but an Amazon-specific increase will be difficult to isolate.

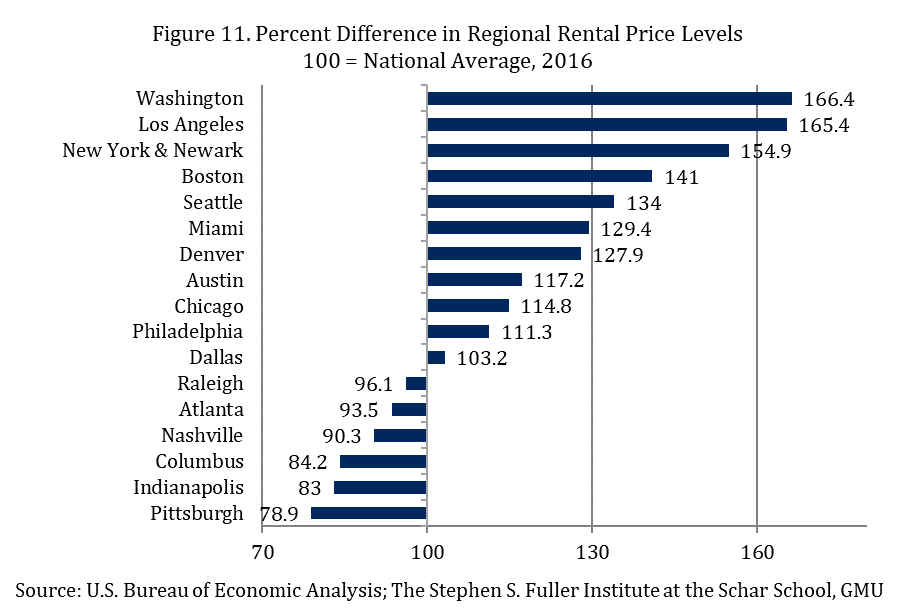

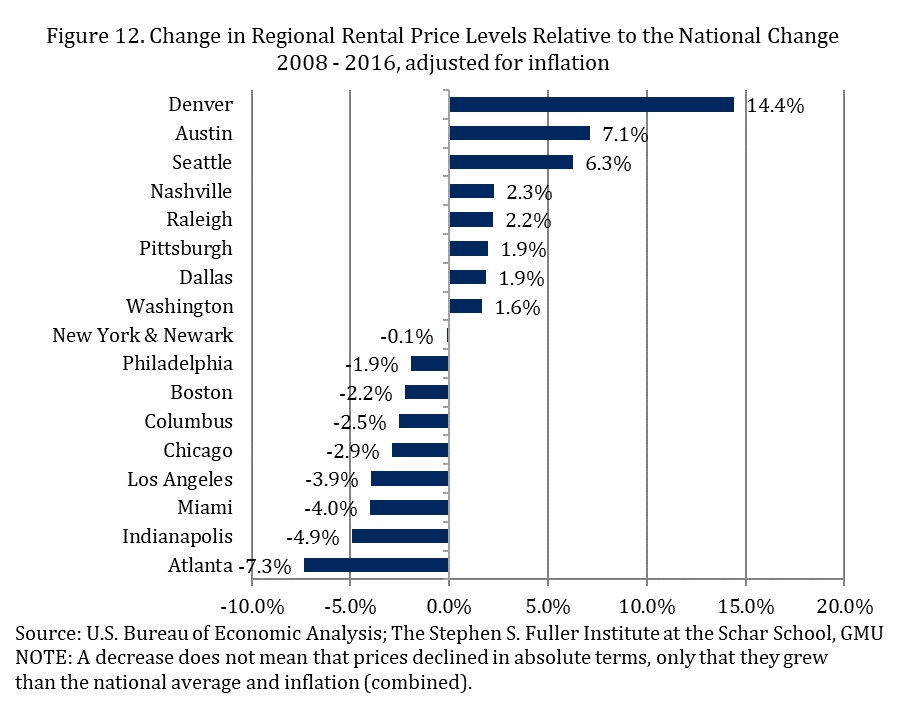

Rents in the Washington region are some of the highest in the nation, and the highest of all the U.S. cities in the 20 HQ2 finalists (Figure 11). Even so, rents have risen only modestly faster than the national average since 2008, ranking in the middle of the pack of the HQ2 contenders (Figure 12). While the underperformance of the region’s economy played a role in, the increase in the rental housing stock likely had a larger effect on pricing. The Washington region’s rents will likely continue to be some of the highest in the nation, with or without HQ2. Because of the relatively large supply of rental housing and, more importantly, the ability for the region to continue to increase this supply, the region’s rental market should be able to accommodate HQ2 households without outsized increases in rents, overall.